Financier Follies?

Self-financing longer dated call option to capture right tail skew.

While that sentence may not accurately describe what a venture capital/private equity investor could possibly see within the prospect of taking a controlling stake in Rangers 2.0, it is a phrase which those type of investors would likely understand.

Today, I will try to explain what that sentence means, and why it could be the kind of thinking which could entice investors like 49ers Enterprises. This is in no way to suggest any particular insight into the likelihood of a deal occurring, but rather, walking through why this type of investor would even be considering.

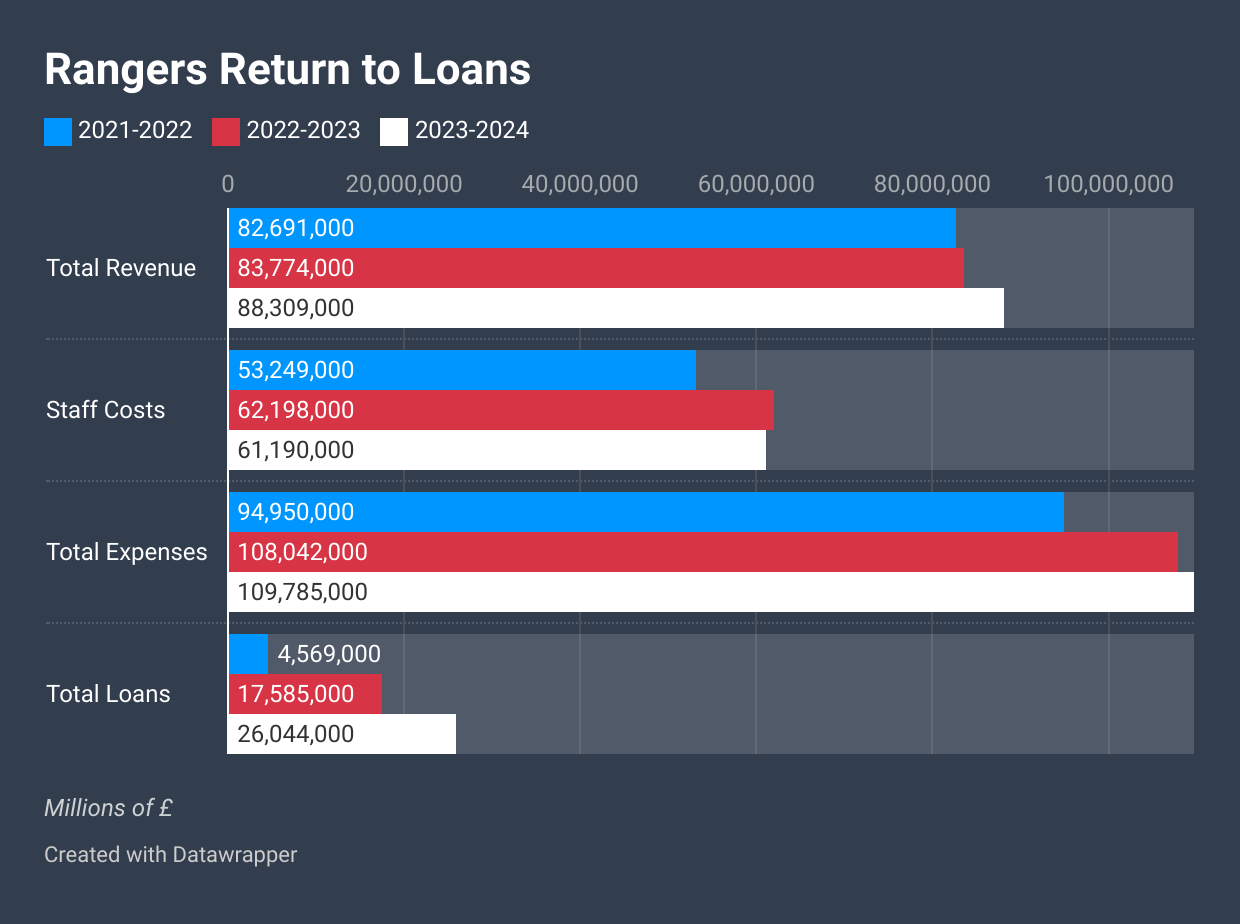

Rangers 2.0 have been very poorly run since they denied Celtic of 10-in-a-row during the 2020-2021 season. Yes, there was the run to the 2021-2022 Europa League Final, but their performance levels within the Scottish domestic game have badly lagged the amounts they have spent on wages. In addition, the two seasons which saw them make that Europa League Final run and the following one with group stage Champions League, had the club’s finances on a potential path to sustainability. Instead, spending was ramped to even exceed that of Celtic, with investor loans piling back up.

These are not reflective of precise accounting standards related to filing requirements, but offer some broad context on the level of operating deficits incurred the past few seasons.

With the deployment by UEFA of FSR, the club hit a wall this season, which has resulted in downsizing and austerity. Even a 20% reduction in the staff cost would not have balanced the books at 2023-2024 rates of commercial activity.

So why would a group like 49ers Enterprises be interested in such a mess?

Keep reading with a 7-day free trial

Subscribe to The Huddle Breakdown to keep reading this post and get 7 days of free access to the full post archives.